By Chantel Gibbs, CPA, CGA, B.Sc, B.A

How to reduce the impact of recent tax changes for your business

If you are a private business owner, you should be aware of the tax changes introduced for the 2019 tax year. While you won’t see the effect of the change until you file your corporate year-end taxes. This article gives an overview of the tax changes, ideas for future financial planning, and some last minute tips for things that can be done before year-end.

The tax changes

In the last two years, the Canadian government has introduced tax changes that have had a large impact on a private company’s ability to pay out dividends to related parties, and that discourages companies from deferring too many earnings in the company or an associated company.

Passive Income

In 2018, the government introduced the tax on split income rules which restricted the ability to pay dividends to any family members who were not substantially contributing to the business. In 2019, it was the reduction of the small business rate based on investment income made on earnings that have been deferred in the company instead of pushed out to shareholders.

Private Canadian controlled companies have a $500,000 small business limit for which any earnings from an active business up to $500,000 are taxed at the 11%[1] corporate tax rate instead of the 27% corporate tax rate. This limit starts to get reduced if the company and any associated companies have a combined worth over $10 million. The new rules also reduce the business limit if the company or any associated companies makes over $50,000 in passive investment income. The reduction is $5 for every $1 of passive income over $50,000 so once there is $150,000 or more of passive income, the entire small business limit is gone.

The effect of this change is not necessarily more tax at the end of the day. If a company loses the small business limit because of passive income, the business earnings are added to the general rate income pool (GRIP) from which low-taxed dividends can be paid. Once all the corporate earnings flow out to the shareholder, the overall tax is about the same whether the company had the small business limit or not.

It can be summarized as follows:

Small business rate = low corporate tax / high dividend tax

General business rate = high corporate tax / low dividend tax

The main impact of the change? Less corporate earnings can be deferred and put into investments when the small business limit is lost because there is more corporate tax up front. There is, however, a less well-known effect and that is on the tax treatment of the investment income itself.

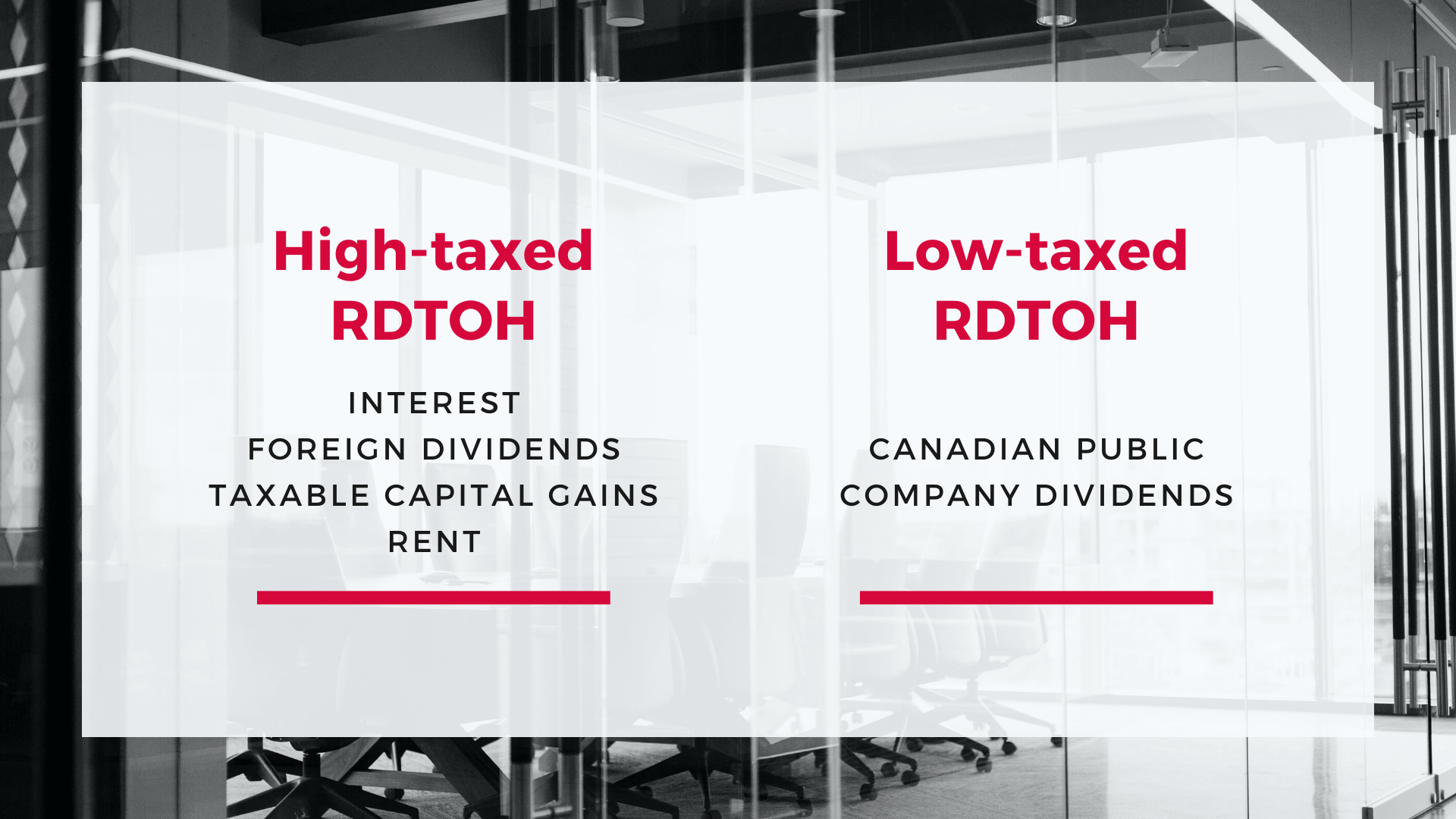

The corporate tax rate on passive investment income in a corporation is much higher than active business income. In BC in 2019, the corporate passive tax rate is 50.67%. Over half of that tax is refundable when dividends are pushed out to shareholders at a rate of $1 refund for every $2.61 in dividends. When all the tax is refunded to the corporation, the effective tax rate on passive income is 20%.

The 2019 tax changes made two pools of refundable tax (RDTOH). One pool can only be recovered by pushing out high-taxed dividends and the other pool is only recovered by pushing out low-taxed dividends. The problem is that the most passive investment income adds to the high-taxed refundable dividend tax pool, not the low-taxed refundable dividend tax pool. The below diagram shows what type of passive investment income adds to which refundable tax pool:

The impact of the changes for your business

It is very possible for a private business owner to have lost their entire small business rate, but still be paying out largely high-taxed dividends because they want to recover the corporate tax on the passive investment income. The GRIP balance in the company (from which low-taxed dividends can be paid) never expires, but depending on whether the company is trying to recover the high-taxed RDTOH pool, the company might end up paying out mostly high-taxed dividends. In that case, the GRIP balance will hardly be used and could even be wasted in the long term.

What you can do to reduce the impact of the new rules

There are a number of financial planning strategies available to help mitigate the impact of these new rules. Some of the financial planning for businesses includes:

1. Stripping yearly earnings out of the company into an Individual Pension Plan or other deferred income instrument;

2. Donating preferred shares of the company to a charity;

3. Using a permanent life insurance policy to have some tax-free asset growth. Leveraging assets, like a life insurance policy’s cash value, so that there is loan interest deducted against passive income

4. Choose investments in the company that produce large capital gains and Canadian public company dividends because those are taxed less harshly.

What you can still do in 2019 to reduce the impact of the new rules

If you want a quick fix for the 2019 year-end, there are less options to choose from. The easiest way is to create more expenses that can be deducted from passive income. If there were capital gains realized in 2019, consider triggering capital losses on other assets to absorb some of the gains.

Call your advisor at ZLC to determine if your financial planning goals align with your long-term financial plans. We work seamlessly with your team of accountants, lawyers and other professional advisors, to ensure the best financial outcome for you.

[1] BC combined small business rate for 2019.

This information is designed to educate and inform you of strategies and products currently available. As each individual’s circumstances differ, it is important to review the suitability of these concepts for your particular needs with a qualified advisor.