By Brent Davis,

Financial Advisor

There is no question that rising interest rates and inflation has been alarming. It’s easy to forget the Bank of Canada’s interest rate was actually 0.25% at the start of 2022. It’s additionally unprecedented for interest rates to have increased as quickly as they have…Nothing about the start of this decade has been normal. While the rollercoaster ride feels like it might never take a pause, the investment environment presents opportunities for investors who can overcome emotional decision making to protect their wealth.

Interest rates are currently at 3.75%. With inflation still elevated, it is likely the Bank of Canada will continue to increase interest rates, at least in the short-term. Here are some straightforward strategies to preserve capital in the face of volatility.

Consider a new kind of savings account

People may be surprised by this, but it’s a worthy consideration. The general rule of thumb is the more liquid, the lower the return. A classic savings account will typically have the lowest rates available. At current rates, the traditional banks might offer 1.3-1.5%.

E-Banks (Manulife & EQ are two examples) can go as high as 2.5%. If you plan on using a savings account, I highly recommend going this route. They are very easy to open and convenient to utilize.

Each bank account comes with CDIC (Canadian Deposit Insurance Corporation) protection up to $100,000. For amounts greater than $100,000, I suggest opening multiple accounts to a maximum of $100,000 for that extra protection.

GICs are another old but new investment option

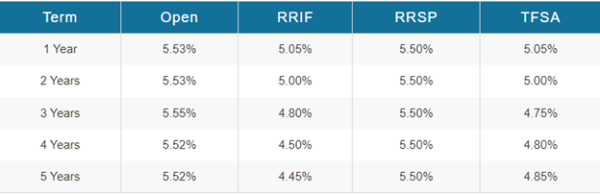

A Guaranteed Investment Certificates (GIC) offers a guaranteed rate of return over a fixed duration. Due to its low risk profile, the return is typically lower than stocks/bonds but higher than a savings account.

Here is a list of the current GIC rates based on account type and duration:

A GIC is undeniably the safest way to receive the highest return. However, as someone that values flexibility, I have a hard time recommending GICs with the exception of 2 situations.

- GICs are a greater part of your overall fixed income/cash strategy in your portfolio

- You know with 100% certainty that you do not need these funds earlier than the fixed time and want the peace of mind.

Do you know about Money Market Funds?

A money market fund is a type of mutual fund that invests in highly liquid, very short-term investments. Due to the large amount of money these funds have, they can invest in short-term securities that the average investor wouldn’t have access to.

Examples of the underlying investments in a money market fund include (but aren’t limited to): government treasury notes and bills, corporate paper, bankers’ acceptances, short-term corporate notes and bank debt securities, and municipal bonds.

If you value liquidity and are seeking higher returns than a savings account, this is your best option. Recent yields can be as high as 3-4% and if rates continue to rise, the yields should as well.

All mutual funds come with an element of risk. Money market funds are rated “low risk” due to the short-term nature of its investments. However, this does not mean there is no risk at all.

Money market funds can “break the buck” providing a negative return to the fund. This can occur when the investment income does not cover operating expenses or investment losses of the fund. Although very rare, this can happen when interest rates drop to very low levels or when the fund uses leverage. Investors should conduct some due diligence to ensure they understand what loans comprise the fund.

Another thing to note – it takes 2 full business days for the trade to settle. Therefore, this strategy should not completely replace a savings account/emergency fund.