Family businesses have a structure that might include the following:

The Parents:

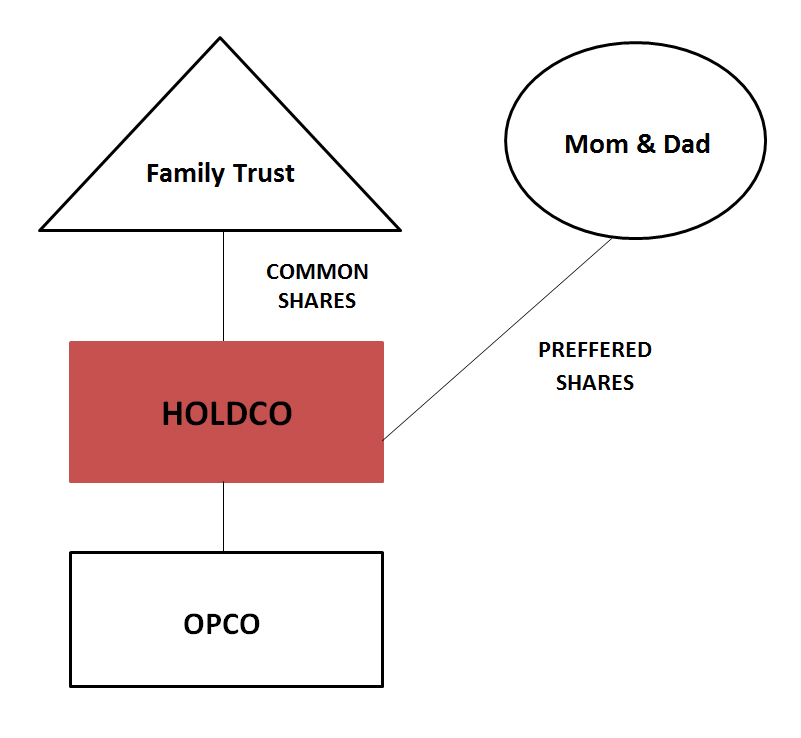

An estate freeze has been implemented and one or both the parents are included as beneficiaries in the trust along with their children.

The parents have retained voting control and their equity has been frozen in preferred shares. They may have adopted the strategy of redeeming preferred shares over time and may have adopted the strategy of funding capital gains tax on those shares with life insurance.

The Children:

The children may not be minors anymore and some of them might have children of their own. Some may be active in the business or management and some may not be. As a result of the freeze, the children are discretionary beneficiaries of a trust that may have developed substantial wealth.

The childrens’ current situation may not reflect the potential wealth that may ultimately flow to them. Also, the children that are married and have families may not be able to provide for those families in the event of premature death.

Issues:

There are two issues in planning for the children that involve life insurance. The first issue is to protect their families and the second issue is to start providing for the future capital gains tax liability related to the assets held by that trust. Another question is how to provide funding for the children to buy life insurance to deal with these issues. The business is the source of the wealth and should probably be the source of the funding to make sure the children and their families are adequately protected. If the children who have spouses are not adequately protected there may be litigation issues that could arise on the premature death of one of the children.

Example:

When there has been a full estate freeze, the value of the new common shares is nominal. All the growth is attributed to the common shares. If the value of the business at the time of the freeze is $5,000,000 and it grows at 7% per year, the common shares are worth about $5,000,000 in 10 years and $15,000,000 in 20 years. The capital gains tax on that value could be very significant.

This area is often overlooked as we often focus on identifying the capital gains tax exposure of the parents and offer solutions for dealing with those obligations. However the next generation can have significant unaddressed issues and need our help to develop solutions. Shouldn’t they be addressed? If life insurance is part of the solution, insurability and cost are at their best in the early years.