Maximum EI benefit increases from 15 weeks to 26 weeks effective December 18, 2022

Fab Biagini, Advisor, ZLC Employee Benefits Solutions

The Federal Government has confirmed that they will be extending EI sickness benefits from 15 weeks to 26 weeks, effective December 18, 2022 (after the 1 week waiting period). At this time, no other changes have been announced so at present we will assume all other aspects of EI continue to apply. However the Federal Government confirmed again that they are still pursuing a broader review of the EI program so further changes may be coming.

What these changes mean for you:

Firstly, there is no immediate action required, so we are recommending that plan sponsors wait for more information before considering any changes. There may be options for employers to consider for both their Short Term Disability/STD (or salary continuance) plan and Long Term Disability/LTD benefits, but there are a number of things to evaluate before making any changes.

Here are two of the most common ways of structuring Short and Long Term Disability benefits and if no changes are made, how this EI change will affect them.

Scenario 1

Employees access EI (for short term absences) and then Long Term Disability benefits after the elimination period of, typically112 or 119/120 days.

- Employees continue to access EI initially, but if the disability continues beyond the LTD elimination period (if less than 182 days), the employee must apply for LTD coverage and notify EI when the LTD claim is approved.

- Typically, LTD benefits provide a higher monthly benefit and therefore it is in the employee’s best interest to apply for LTD as soon as it becomes available.

- Employees are not eligible to receive both EI and LTD benefits at the same time.

Scenario 2

Employees access Short Term Disability benefits (or a salary continuance plan) and then Long Term Disability after the elimination period of 112 or 119/120 days.

- There are no changes required as EI does not impact either benefit.

- Note; if you currently qualify for EI Premium Reduction Program (PRP), this will continue for now with no changes.

Regarding PRP, the government hasn’t yet provided any details about the new qualification criteria for the PRP or the transition period. However, they will likely introduce a legacy clause to give plan sponsors enough time to make the necessary changes to their plans to ensure they remain eligible for it.

Regarding Scenario 1 above, one option plan sponsors may consider is to extend the LTD elimination period to begin after the new EI benefits ends (26 weeks). With this change, we would expect to see LTD premiums reduce slightly. However, this will be based on the particulars of the specific plan sponsor and insurer. Before making this change, plan sponsors should consider any contractual obligations, collective agreements and the impact to employees.

Regarding the impact to employees, extending the LTD elimination period may negatively impact the employee’s disability benefits. Here’s why:

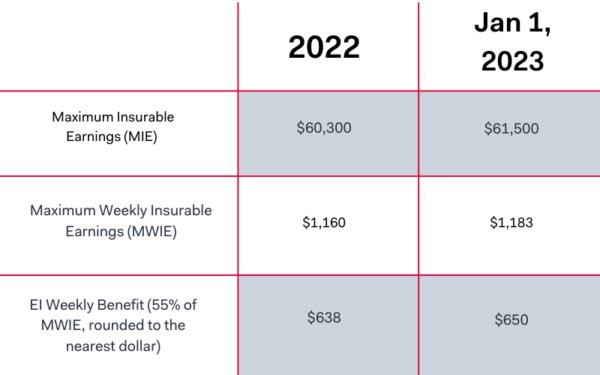

EI benefits provide 55% of the Maximum Weekly Insurable Earnings (MWIE) up to $638 for 2022 (taxable income) – see changes below for January 1, 2023. LTD benefits most commonly provide 66 2/3% of monthly earnings (non-taxable income as employees pay the premium). Here’s how compensation calculates for EI versus a common LTD benefit plan (based on the new 2023 maximum):

For more details about the change: https://www.canada.ca/en/services/benefits/ei/ei-sickness.html

If you would like to discuss this further, please contact ZLC Employee Benefits Solutions. We will contact you should more details be provided, and any immediate action is required.

Maximum Insurable Earnings increasing January 1, 2023

If your policy is currently set to match the EI maximum, your policy will automatically increase to $650 on January 1, 2023 and therefore you will continue to qualify for the EI Premium Reduction Program (PRP).

If your policy does not, and provides a weekly benefit lower than $650, you must contact us if you’d like to increase your benefit in order to continue to qualify for the EI Premium Reduction Program (PRP).