Diagnosis of a critical illness is a life altering moment, not only for the individual with the diagnosis but also for their entire family. Although our health care system generally provides treatment at no cost, there are often unforeseen costs associated with a critical illness diagnosis that can decimate a family’s life savings.

Research indicates 1 out of every 3 Canadians will likely contract a life-altering critical illness during their lifetime.1 While life insurance is frequently bought to protect loved ones, the possibility of not being able to work and provide for one’s family because of critical illness is often not considered.

What is Critical Illness Insurance?

Critical Illness insurance provides a lump sum cash tax-free benefit upon diagnosis of a critical illness. This benefit is generally paid out upon the individual surviving 30 days after diagnosis.

Which Conditions are Covered?

Basic coverage typically includes protection for life threatening cancers, heart attacks, and strokes. More comprehensive coverage often includes protection for some or all of the following conditions: Aortic surgery, aplastic anemia, bacterial meningitis, benign brain tumor, blindness, cancer (life threatening), coma, coronary artery bypass surgery, deafness, dementia, including Alzheimer’s disease, heart attack, heart valve replacement or repair, kidney failure, loss of limbs, loss of speech, major organ failure (on waiting list), major organ transplant, motor neuron disease, multiple sclerosis, occupational HIV infection, paralysis, Parkinson’s disease and specified atypical parkinsonian disorders, severe burns, and stroke.

How Does a Critical Illness Policy Work?

Critical Illness insurance can be purchased for a specified term (i.e., 20 years) or permanently (until your death). If you are facing a medical crisis, the insurance money can help you in many ways such as:

- Obtain additional treatments not covered under provincial health care

- Pay for medical equipment, supplies and other recovery costs

- Supplement your income if you are unable to work

- Modify your home and adapt your lifestyle (i.e., wheelchair ramps, grab bars)

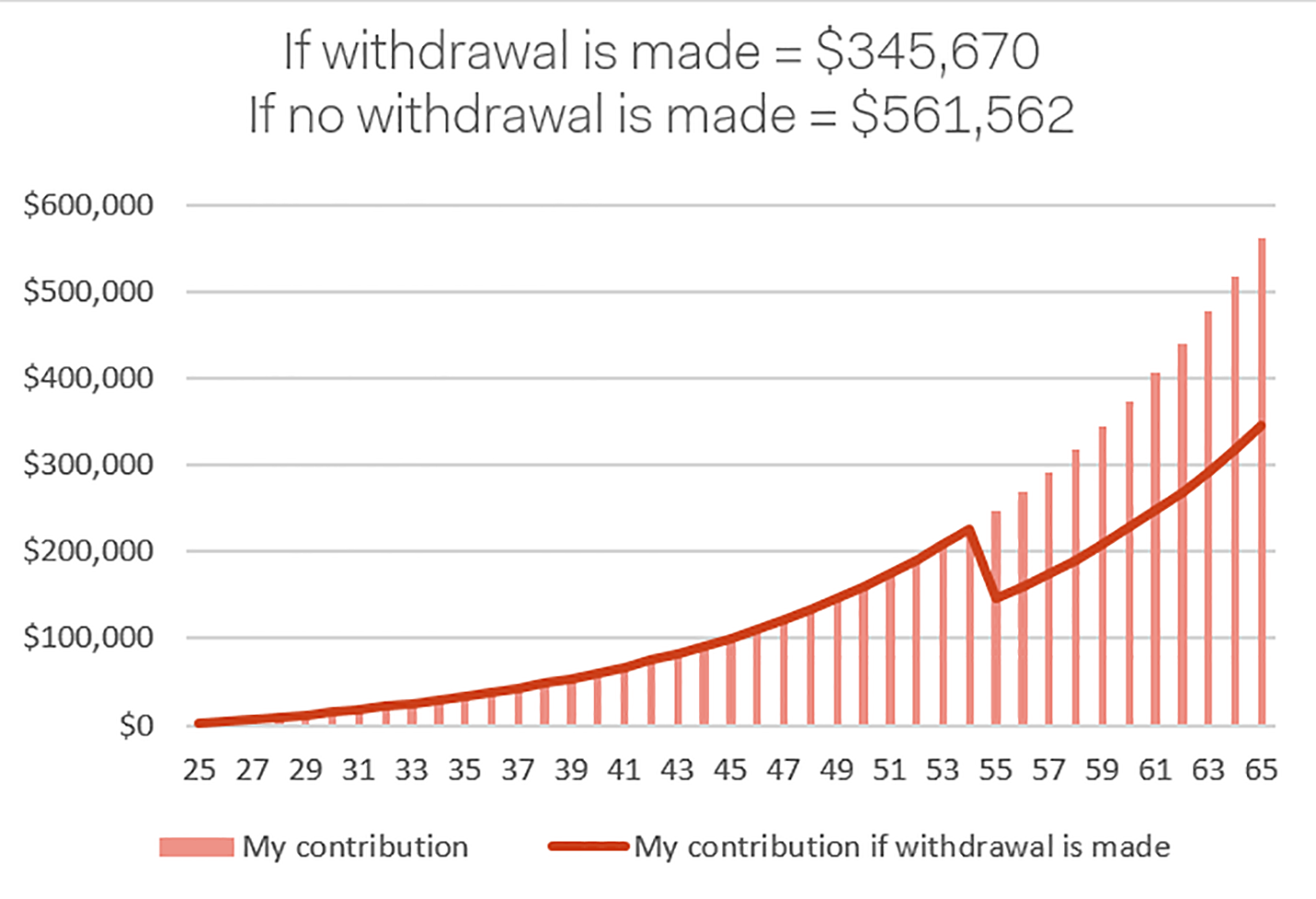

Critical Illness Impact on Savings

Scenario: 55 years old; diagnosed with life-threatening cancer; and withdraws $100,000 from RRSP to pay for private treatment and loss of income

Impact: Almost 60% reduction in projected available retirement savings/income

At ZLC, we believe that our clients can make the best decisions when they have been given the most comprehensive expert advice possible. Every individual’s circumstances are unique to them and therefore it is important to review your particular needs with a qualified Advisor.